Canada leads the way globally as a preferred immigration destination. Every year, hundreds of thousands of hopeful people apply to immigrate to Canada. However, understanding Canada’s many immigration programs can be confusing. Many people rely on consultants for help to immigrate to Canada. However, it’s important to understand how to select an immigration consultant. Discover what to know and how to avoid immigration fraud.

1. Apply Directly to Immigrate to Canada

The primary way for skilled immigrants to live permanently in Canada is through the Canadian Government’s Express Entry program. There are three immigration programs under Express Entry, and each has different requirements.

Advertisement:

You can visit the Government of Canada site to see if you are eligible for Express Entry. It takes about 10 – 15 minutes to find out if you are eligible and answer questions about your:

Nationality

Age

Language ability

Family members

Education

Work experience

Details on any job offer (if applicable).

What Happens After You Complete the Eligibility Questions?

Advertisement:

After you respond to the questions, you will:

Be advised if you meet the eligibility requirements to immigrate to Canada

Receive a personal reference code

Be provided with the next steps you need to follow.

When you complete the steps, you will receive a confirmation that your profile is complete.

The Canadian government determines how many Express Entry applicants will be admitted to Canada each month.

2. Apply with an Immigration Consultant

You can also hire an Immigration Consultant to help you apply to immigrate to Canada. An experienced consultant knows about the many streams and programs available for people looking to immigrate to Canada. With more than 100 Canadian immigration programs, they can help you select the right program.

What to Know if You Hire Someone to Help You Immigrate to Canada

The Government of Canada has important tips if you decide to hire a representative to help you with your immigration process:

Advertisement:

To Find a Paid or Unpaid Representative:

Ask people you trust to recommend someone. Be sure to get advice from several people before you choose.

Ask questions. Be careful of someone who won’t answer your questions.

If You Hire a Paid Representative:

Immigration consultants must be licensed by the College of Immigration and Citizenship Consultants. Review these helpful tips to ensure you select a qualified representative.

This means they have a license to practice and give advice.

If you choose a paid representative who’s not authorized, the Canadian government may return your application or refuse it.

If you give a representative money or compensate them in any other way in exchange for their services, they’re considered paid and must be authorized.

2. Ask the representative about their training and experience.

3. Find out how long they have been in business and ask for references.

4. Discuss the services they provide and their fee.

5. Get a written contract and read it carefully before you sign it. Ensure the contract lists all the services they will give you and clearly states the fee you discussed.

Also, if you use a representative who works in Canada, you can contact the Better Business Bureau (BBB). The BBB can tell you if they have received complaints about a citizenship or immigration consultant, lawyer, or other representative.

Tips to Protect Yourself from Fraud When Immigrating to Canada

If you plan to immigrate to Canada, it’s vital to avoid fradulent activity. Immigration fraud can have devastating consequence from delays to deportation. Here are some tips to avoid the risks:

Be careful of anything that sounds too good to be true. The Canadian government advises that using a paid representative will not draw special attention to your application or guarantee they will approve it.

Beware of representatives who encourage you to give false information in your application. Providing false information is against the law, and you could be denied entry into Canada or deported after you arrive.

Don’t leave original documents or photos with your representative.

Don’t sign blank application forms.

Read any forms or documents carefully before you sign them. If you don’t understand them ask someone to translate.

Get copies of any documents your representative makes for you.

Get a signed receipt for any services that you pay the representative for.

Make sure your representative updates you often about your application.

Protect your money and remember that the Canadian government will never:

Call you and ask you to deposit money into a personal bank account

Ask you to transfer money through a private money transfer company.

Only ask for processing fees in Canadian dollars and the fees are the same around the world.

It’s smart to make a checklist of the important documents to carry when you move to Canada. Whether you are immigrating permanently, studying, or working in Canada, these documents will help you to enter Canada, open a bank account, drive, rent a house, and even access healthcare. This comprehensive list of documents outlines what you will require and why you need them. Ensuring you have the right documents for permanent residence (PR) can minimize delays and avoid complications as you settle in Canada. Without the right documents, you may face challenges finding a job, enrolling your children in school, or even renting a place to live.

It’s important to keep all your documents safe and keep digital copies.

Advertisement:

Essential Documents for PR in Canada

You will require specific documents to complete the immigration process and PR in Canada. The PR documents you require vary based on the immigration program you’re applying for. However, here are some of the essential documents you will need.

Passports and Birth Certificates

Advertisement:

Passports show your biographical information for you, your spouse or common-law partner, and dependent children. Passport photos must comply with Canadian passport photo specifications.

You’ll need a birth certificate or an equivalent document from your birth country for yourself and each family member travelling with you. Birth certificates serve as proof of your date and place of birth. If you do not have a foreign birth certificate, the date of birth indicated on your foreign passport or travel documents will establish your date of birth. You will need a birth certificate to get a Social Insurance Number, enroll your children in school, or apply for government services.

Adoption Certificate

If you identify a dependent child as “adopted” you will require a certificate from a national authority to show that the adoption is legal and approved.

Marriage Certificate (or Divorce and Legal Separation Agreement)

If you declare yourself married, you will need a valid marriage certificate issued by a government authority under the law of the country where you were married.

A divorce certificate and legal separation agreement are necessary if you declare your marital status divorced.

Advertisement:

Education and Professional Documents

Carry your educational certificates and official transcripts. These documents prove your education qualifications and you may require them to attend Canadian schools or for employment. And, don’t forget any school records you have for your children!

Post-secondary Diplomas, Degrees, and Academic Transcripts

You may need an education evaluation or credential recognition from an evaluation service, academic institution, or professional association. Such evaluations can help you to find work more easily. You may also require them if you plan to work in a regulated occupation or attend post-secondary schools in Canada.

Many professional associations, universities, colleges, and assessment agencies require the school you attended to send your academic records directly to them. They may not accept the original or a copy of academic documents. You may have to get your documents translated into English or French, depending on the language requirements of the province you are moving to. It’s a good idea to find out what documents the professional association, academic institution, or credential assessment agency requires before you come to Canada. This will also save you time and money and avoid costly delays.

Samples of Your Professional Work

It is helpful to bring samples of your professional work to showcase when you attend job interviews in Canada. Bring your resumé or curriculum vitae. However, you may have to use your existing resume as the foundation to write a Canadian-style resume.

Reference Letters from Former Employers

Canadian employers often request references from former employers before they offer you a job. So, it’s helpful to bring reference letters with contact information. An official reference must be a printed letter on company letterhead and include:

Company contact information (address, telephone number, email)

Name, title, and signature of the immediate supervisor/manager at the company

All positions held with job titles, duties, and employment start and end dates.

Your Child’s Education Documents and Records

If you have young children who are immigrating to Canada with you, consider carrying their education documents as well. Your children may have to complete a math and English language skills assessment when you enroll them in school. The assessment results will identify what grade level your child is at and what support they may need to achieve success in school. It’s helpful if you can provide your child’s previous report card or other documents to help place them into the right grade.

Continuing to care for your health when you move to Canada is vital. Health-related documents such as medical records, vaccination records, prescriptions, etc, are helpful when you seek a medical doctor or apply for health insurance.

Medical Records

If you need to complete an International Medical Exam (IME) it’s helpful if you can bring any medical reports or test results for any previous or existing medical conditions.

Most people seeking permanent residence in Canada will require an IME. If you do not have adequate immunization records, you may have to start an immunization schedule based on your age and risk factors. This applies to adults and children. Immunizations are not mandatory in Canada. However, children and adolescents who attend school in Ontario and New Brunswick must have proof of immunization.

For the IME, it is not mandatory to show proof of vaccination. However, proof of previous vaccination is helpful, including vaccination against illnesses such as tetanus, pertussis, measles, mumps, COVID-19, and others.

Travel Health Insurance

While you can apply for public health insurance when you arrive in Canada, some provinces have a waiting period before you can receive provincial health care coverage. Buying private health insurance to cover expenses in case of a medical emergency during your first few months in Canada is a smart idea. Without medical health insurance, you could face a large bill for medical treatment or emergency surgery. Having to pay a hefty medical expense is not how you want to begin your new life in Canada. It’s much better to purchase insurance for peace of mind.

Financial Documents and Proof of Funds

Proof of funds show you have enough money to support yourself for at least the first three months in Canada. It can take three to six months to find a job in Canada, and you will need to have money for living expenses until you have a stable income.

Certificates of Valuation and Authenticity for Jewellry and Valuables

You’ll need a list of effects when you land at the airport. It’s also helpful to have certificates of valuation and authenticity (including photos) for jewelry, valuables, and belongings you carry. You can read more in Goods to Follow | Bringing Your Goods to Canada.

Record of Foreign Income, Properties, or Investments

Foreign income is taxable in Canada.

Canada PR Documents You Require When You Land

When you land at the airport in Canada, you will meet with an immigration officer from the Canada Border Service Agency (CBSA). The officer will check that you enter Canada on or before the expiry date on your Confirmation of Permanent Residence (COPR); this date cannot be extended. If there are no problems, the officer will authorize you to enter Canada as a permanent resident.

When landing at the airport, you require your:

Passport or travel documents

Confirmation of Permanent Residence (COPR) for you and any dependents travelling with you

CBSA declaration card

List of any goods you have with you and a list of goods to follow

Proof of funds.

While the immigration officer may not ask you for proof of funds, it’s helpful to have.

The officer will also confirm your Canadian mailing address. Your Canada permanent resident card will be mailed to the address you provide. You can notify IRCC if you change your address before you receive your PR card using this online address notification service. The time to process your PR card can vary. However, you can check the IRCC website for current processing times.

If you plan to drive in Canada, you can get an International Driving Permit (IDP) from your home country. Permanent residents can use the IDP for a defined period (usually 60 – 90 days depending on the province). Be sure to check the specific IDP requirements of the province you are moving to. Some provinces in Canada may allow you to exchange your foreign driver’s license for a Canadian driver’s license, while others may require you to take a driving test.

International Automobile Insurance

If you have a good driving record in your country of origin, you may be able to get a better auto insurance rate in Canada. Bring a copy of your international automobile insurance to show your driving record.

With this comprehensive list of documents for PR in Canada, you can begin to gather and organize them for your convenience. Having these documents before you move will minimize potential delays and help you settle when you arrive.

A lesson many newcomers learn when they arrive in Canada is that you need credit to pay for large expenses, buy a car, or purchase a home. However, it’s difficult to borrow without a credit history in Canada. Canadian lenders typically check each applicant’s credit files at one of the main credit reporting agencies (Equifax Canada and TransUnion). This file is like a financial report card that tracks how much you borrow and how quickly you pay it back, to calculate your credit rating and credit score.

Without a credit history, newcomers may need a loan co-signer with a Canadian credit rating, and considerable assets as collateral, or they must demonstrate a history of stable income in Canada to receive a loan. Fortunately, you can start to build your credit record and history shortly after you arrive in Canada.

Advertisement:

Getting Started

The financial decisions you make when you arrive in Canada have a huge impact on your credit history and score. The concept of credit can sometimes lead to a debate about how it can help, or hurt you when you are building your credit rating. On one hand, credit can be a fantastic tool to help you:

Get a loan or a mortgage

Save on credit card and loan interest rates

Get approval for lines of credit

Obtain certain jobs (i.e. some finance-related roles will require a credit check as a condition of employment)

Rent a home.

Advertisement:

On the other hand, if poorly managed, credit can haunt you for many years, and make you miss out on financial opportunities. Creditors can run a credit check on you to assess if you are a low-risk or high-risk borrower. They will also decide to grant or deny you a loan or charge you a higher interest rate.

What is Credit History?

Your credit history shows lenders that you are responsible when it comes to paying your financial obligations. Whether that is your monthly rent, utility bills, loans, etc. If you have come from a country where you have credit bureaus, you know how important your credit history is. Maintaining a good credit history in Canada is also important.

We’ll share tips to help you build and maintain a healthy credit report. With a strong credit history, you can save money and have more financial freedom.

So what is your credit score when you come to Canada? Nothing. Think of it as a blank slate. Everything you do henceforth will dictate what direction your credit rating will go, up or down.

Your credit history or credit rating starts the first time you get a credit card or loan in your name from a Canadian bank. You can begin by applying for and using a credit card responsibly.

Even if you don’t have immediate plans to buy a house or vehicle, it’s good to establish a credit history, since banks may give special consideration to recent newcomers.

Newcomers may be eligible for a ‘secured’ credit card. A secured credit card is different than a regular credit card because it requires a security deposit equal to the amount of the credit limit. Think of it as a stepping stone to getting an unsecured credit card. Such special offers may be more difficult to obtain later, especially if your income does not grow as fast as you had hoped. A credit card is also useful for larger purchases and as a secondary piece of identification.

Why is Your Credit Score Important?

Your credit score is important for several reasons:

Lenders will review your credit score when you want a mortgage to buy a home, or a loan to buy a car. They want to understand your payment history, and your ability to manage credit and pay off debt.

2. Landlords will conduct a credit check before renting their property to you.

3. Some employers will conduct a credit check before they make an offer of employment. This is common with banks and other financial institutions such as insurance companies.

What Credit Score is Good?

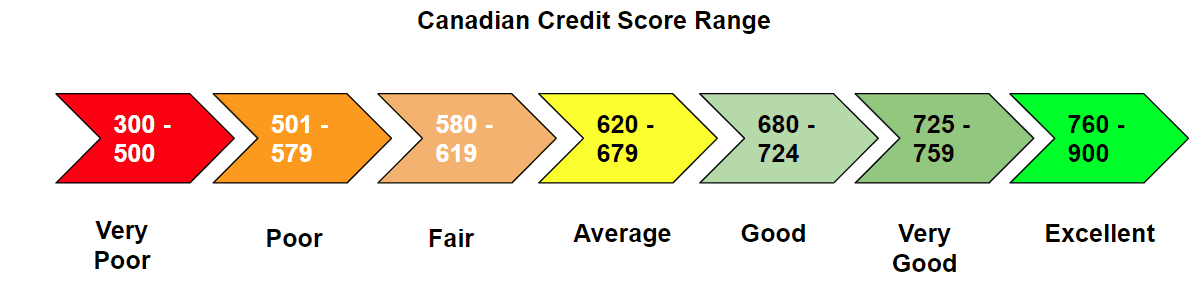

Your credit score can fall between the range of 300 – 900. Generally, and depending on the credit score model that your financial institute is using a good score is greater than 680. As a benchmark, to get a mortgage to buy a house in Canada, you need a credit score between 600 – 700. If your credit score is lower than 600, you will want to take steps to increase your credit score.

Once you receive a credit card, use it wisely to establish a credit score so that lenders will have confidence in your ability to repay loans.

Your credit is scored on a point system that ranges from 300 – 900 points, where 900 is the best score. To qualify for a loan, your score should be 650 points or higher. If you score lower than 650, it may be difficult to get a loan or receive new credit. However, if you have a low credit score, you can improve your score by carefully managing your credit use.

How Much Credit Limit Should I Use?

If possible, avoid using more than 30% of your credit limit (balance-to-limit ratio). For example, if you have a credit limit of $1,000, you should try not to spend more than $300 and pay the bill in full by the due date.

Your credit score may decline if your balance-to-limit ratio exceeds 30% as it may indicate to creditors that you are a higher-risk borrower.

How Many Credit Cards Can I Have?

It’s best to start with only one until you are financially comfortable enough to afford more. Avoid opening many credit accounts. Many credit card accounts can signal financial distress to lenders, especially if they all carry a balance on them.

Why Credit History is Important to Rent a Home in Canada

Your credit history is one of the things landlords want to see before giving out their home to you. Your credit history will tell the landlord how reliably you pay debt. A good credit score will tell the landlord that you are reliable and will likely pay your rent on time. This is important to landlords as it guides them in their decision regarding who to rent their home to and who to avoid.

While this arrangement is great for landlords, it can be problematic for newcomers who are looking to rent a home. If you are a newcomer to Canada, you likely will not have a credit history. It takes a minimum of six months to build a credit history. Because of this, it can often be hard to convince a landlord that you will be a reliable tenant. However, there are some tips that you can follow to rent a home without a credit history.

How Do I Rent a Home Without a Credit History?

The first thing you can do is show proof to your future landlord that you have a good amount of savings in your bank account. This will tell the landlord that you have enough money to pay the rent and will pay it on time.

If you don’t have a good amount of savings, your top priority would probably be to secure a source of income. Once you have done that, you can show proof of income to your landlord. This will also satisfy landlords because it means that you have enough money coming in every month to pay the rent.

There is also another way to get a house on rent without a credit history. Some landlords openly accept newcomers and reserve their homes, especially for newcomers. These rentals may be small and less than ideal. However, they are a good option if you need a place to stay while you build your credit score. Many times, these rental homes have basic furniture like beds and sofas which makes it easier for newcomers to move into.

In the meantime, paying your bills on time and being reliable with all of your payments is a great way to show lenders that you are financially responsible. And over time, you will build a strong credit history that will provide many financial benefits.

How Do I Maintain a Good Credit History?Five Tips to Follow

1. Take Advantage of Your Fresh Start in Canada to Build a Good Credit History

Get a credit card or two, and use them, but use them sensibly. Pay off your balance each month and avoid going over your balance to show potential lenders your reliability.

Paying in full each month will also reduce the amount of interest you pay. And with the average credit card interest rate at approximately 19%, any balance on your credit card can become very expensive. But, if you don’t pay the balance in full each month, be aware of the interest rate charges.

If you can’t pay the full balance on your credit card, at least pay the minimum balance and make regular payments, to pay off debts as quickly as possible. But, avoid missing payments. Missing payments can damage your credit score and make it difficult to get a future loan such as a car loan, or mortgage.

Using your credit card for cash advances is even more expensive. Typically, the interest rate is higher and you pay interest from the date of the cash advance. There is no grace period like there is for a regular credit card purchase.

2. Read the Small Print on Cancellation Fees and Penalties

On top of paying your monthly bills and loan installments on time, you need to be careful when you sign up for services such as cable, telephone, internet, gym subscriptions, and other monthly subscriptions. Check the cancellation fees and deadlines when you sign up for such services. Otherwise, these fees can be high.

Be sure to ask questions about your contract if there is anything that you do not clearly understand.

3. Keep Track of Your Utility Changes

When you move, don’t forget to cancel or transfer your services and utilities to your new address. Sometimes final bills end up in collections out of sheer neglect, and from collections, they land on your credit report for the next six years. Always keep track when you make such changes, by recording the date, the names of the agents you speak to, and your case number. Or, if you are given a receipt, be sure to hang on to it to prove that you cancelled the service.

4. Negotiate a Payment Schedule with Creditors if You Hit a Rough Patch

If you hit a rough patch, such as an extended period of unemployment, do not be complacent about your credit. Call your creditors and negotiate your monthly payments. They will likely be willing to help you because sending outstanding accounts to collections would cost them more money. Cancel or suspend services you can do without, rather than have the bills rack up.

It’s wise to live within your financial means. As the saying goes, “It’s not how much you earn, it’s how much you spend.”

5. Use Services to Track Your Credit History and Maintain a Good Credit Report

Most banks including Scotiabank offer account holders this facility. Alternatively, use free services like Borrowell to monitor your credit. If you notice outstanding payments that you have paid off on your report you should inform the reporting agency in writing so that this may be removed.

What’s in Your Credit Report?

Credit reporting agencies such as Equifax and TransUnion Canada record your credit history. Your credit report will contain information on your:

Loans

Credit accounts

Bills (for example, outstanding cell phone bills can be listed on your credit report)

Collections items (for example, if an outstanding debt is sent to a collections agency), and

Legal items (for example, if a court order is issued against you for an outstanding debt).

Collections items stay on your credit report for six years, and legal items stay for ten years. So it’s essential to practice good financial habits that don’t jeopardize your credit rating.

Your credit history speaks volumes to lenders about what kind of risks they take when they agree to lend you money. It takes a long time to build a credit history. Yet, it’s easy to sabotage and takes even longer to rebuild.

So, can you live without credit? Yes. But, should you try to do without it? No. Because without credit, it will be difficult to improve your living standards, at the very least, not as quickly as you would like. And, when it comes to making major purchases such as buying your first home in Canada, a strong credit report is essential. When you manage how you use credit, you’ll remain in good financial standing and be able to secure credit to achieve your important dreams.

For newcomers, carefully managing your finances is vitally important, especially if you have not yet landed your ideal job. And, settlement agencies suggest that it can take up to six months to land a job that matches your skills and experiences. In the meantime, managing your finances and spending can serve to reduce stress and financial pressure. In addition, managing your finances well will help you build your Canadian credit history and influence your credit score. Here, we’ll explore how you can create a budget for some of the main expenses you will have to cover in Canada. So where to start, which is essential to achieving future loans! You need to establish your Canadian credit history because it will be important for many reasons including buying your first home.

One of the most important factors in your financial situation is not how much you earn, but rather how much you spend. But, many Canadians get caught in too much debt, trying to “keep up with the neighbours” — in other words, buying everything you want, from cars to electronics, even if you can’t afford it. Overspending can get you caught in a trap that you want to avoid.

Advertisement:

Create a Budget to Manage Your Personal Finances

To manage your personal finances, you can prepare a budget. with the following costs in mind. But the cost of living in Canada depends greatly on the city in which you choose to settle and on the size of your family. Large cities attract the bulk of new immigrants and offer the most job opportunities, however, living costs are also higher. Here are some of the basic expenses that you can keep in mind to help you manage your finances:

Rent Payments

Advertisement:

Newcomers often rent an apartment as their first means of accommodation. Typically, rent prices for a small one-bedroom apartment begin at $700 and can be as high as $2,500 per month depending on the city you choose to settle in.

When renting, make sure that you conduct thorough research on the apartment building and its surroundings and then outline the positives and negatives to see if it is the right place for you. Perhaps the property is close to amenities like shops, swimming pools, libraries, and public transport which depending on your requirements may make it an attractive option for you.

Our Rentals for Newcomers site is a practical and easy-to-navigate site that can help you find housing that meets your unique needs! And you can even determine the average costs of rentals in cities across Canada. This is helpful since rental prices change often. You’ll also find some helpful articles related to housing in Canada.

You will need to budget for the cost of utilities such as electricity (hydro), heating, telephone, cable, and internet.

Many rentals include heating and some include even hydro in the cost of the rent. If you have to pay for electricity, you can ask the landlord what you expect to pay every month. But, your bill will also depend on usage and time of day.

When it comes to internet, cable, and telephone, the best option is to shop for bundles (combined service plans) from different telecom providers in your area. A bundle can cost anywhere between $60 per month to more than $100 per month. Or, check out streaming services that can be less expensive than cable television.

Cell phone plans range from $15 per month to more than $150, depending on the number of free minutes and text messages and the data usage limits. Voicemail activation usually costs extra. You can start with a basic plan and upgrade according to your needs.

While not a bill per se, the cost of doing laundry will be similar from one month to the next. Apartment buildings come with laundry rooms with coin or card-operated washing machines. A washing cycle costs between $2.25 to $3.50 depending on the length, and a dryer cycle has a similar cost.

Even if you are renting, it’s a good idea to purchase renter’s insurance to protect you against damage and theft. The insurance can cost up to a few hundred dollars a year. Auto insurance is $1,000 or more a year.

Depending on your province, you may also have to pay health insurance premiums, which vary from province to province and according to the size of your family. You will also need to factor in the premiums for any private health insurance you may choose to buy.

Public transit is probably the most affordable to travel within your city. And, all cities offer affordable travel options such as buses, trains, subways, light-rail trains, and streetcars. A monthly transit pass can cost anywhere between $70 to more than $150 depending on the city and the number of travel routes that it covers. In large cities, such as Toronto, the public transit system covers the broader Greater Toronto Area, and you can easily transfer from one mode of transportation to another.

To use public transit, you can purchase individual tickets starting at $2.50, but you can use a transfer at the start of your destination to transfer to different modes of transportation. In other words, you only have to pay once at the start of your destination. You can also buy transit passes that allow you unlimited transit use for a period of time. Some cities offer an electric fare payment system that allows you to load money onto a card to make travelling easier and at a discounted fare.

You can find specific fare information about public transit in your city by visiting the website of your city government, or the public transit system.

Food and Other Groceries

The cost of your food bill will depend largely on your dietary limitations and personal standards, but also on the area in which you live. The stores and supermarkets in popular posh areas will be more expensive and will offer more high-quality gourmet and organic products, while cheaper areas will have more low-cost options. Food can set you back anywhere from $100 per month for a single person to several hundred. Cooking at home and planning your meals will help to balance cost and nutrition.

In terms of personal care items and other supplies, costs can start at $1 at dollar stores, but you will often have to compromise on quality. Supermarkets have their own store brands that are usually cheaper than name brands and, in many cases, of comparable quality.

Clothing

Again, your personal standards will have the final say when it comes to clothing. You should bring with you quality items that will last you for a while because clothes shopping is best kept until after you find employment. You can pay anywhere from a few dollars for an item of clothing at a cheap retailer or a thrift (second-hand) store to hundreds and even thousands at high-end designer stores. Read more about the types of clothing you’ll need in Canada.

Entertainment

Movie tickets can cost from $7 to $15 depending on the movie and the time of day. Most theatre tickets usually start at $20, and concerts of popular performers can cost well over $100. You can take advantage of local libraries to borrow DVDs and look for community theatres with free performances or performances by donation. It’s important to budget for entertainment, but this may be a personal finance area that you can cut back on if necessary.

Other Personal Finance Expenses

Big cities can be very tempting with their variety of cultures and cuisines, so you will probably want to treat yourself and your family to occasional restaurant outings. The costs can be anywhere from a few dollars per person at fast-food restaurants, to more than $50 per person at an average restaurant. Never forget to factor in the tip, which should be at least 15 to 20 percent of the bill.

Staying fit and healthy should always be a priority. Some rental buildings come with their own gyms and the price may be very low or included in the rent. If you plan to subscribe to a gym, always read the fine print. The monthly cost is usually $60 to $100, but most gyms charge introductory fees and substantial cancellation fees.

Personal care costs also cover the range from basic to luxury. Expect to pay at least $25 for a simple haircut (plus tip) and anywhere from $40 to $60 for a manicure.

If you’ve recently arrived in Canada, managing your personal finances carefully will help you to reduce financial stress until you find your first job. And, the strong personal finance habits that you follow during your first year in Canada will help you to achieve many of your long-term financial goals.

Are you looking to buy a franchise in Canada but are unsure if you can afford the costs? It’s true, an average middle-class salary alone probably won’t be enough to make your dream a reality. But, that doesn’t mean starting a franchise is impossible even on a limited budget. You just have to know where to find the help you need.

Franchise Start-Up Costs

Start-up costs vary widely and can range from as low as $10,000 to more than $1,000,000. A big factor is whether or not you need to own own or lease real estate for your franchise business. You can find the cost to open a franchise in the franchisor’s Franchise Disclosure Document (FDD). Item 5 contains the initial or franchise fee, or the cost to join the franchise system. Item 7 lists additional start-up costs required such as real estate, equipment, inventory, signage, business licenses, and insurance.

Advertisement:

You will also want to include a budget for professional fees for accounting and legal advice. It’s vital to speak to a franchise lawyer and financial advisor/business accountant before you sign a franchise agreement. They can help you to identify any legal or financial issues that may not be in your best interest.

How Much Can You Afford to Buy a Franchise?

Advertisement:

To determine how much you can afford to invest in a franchise, you need to have a good understanding of your current finances. You can start by determining your net worth by compiling a balance sheet that lists all assets and liabilities. Some franchise experts advise that you should not invest more than 15% of your own money, but this percentage may vary. When you work with a financial advisor, they can help you determine how much of your own money you can afford to invest based on your financial situation.

Unless you are interested in a low-cost franchise, you will likely need to borrow the majority of the funds to purchase your business. In general, lenders require you to provide 20-25% of the total investment. For example, if you have $50,000 to invest, you can research franchise opportunities in the $200,000 range. Before you approach any lender, make sure you are current on all bill payments and correct any mistakes on your credit report.

How to Calculate Your Net Worth

It’s really quite simple to calculate your approximate net worth in three simple steps:

STEP ONE:

STEP TWO:

STEP THREE:

List your assets (what you own). This may include your:

– Savings – Retirement accounts – Market value of your house and car.

List your liabilities (what you owe). This may include your:

– Mortgage – Outstanding loans – Credit card debt

Subtract your total liabilities from your total assets and you’ve just calculated your approximate net worth.

Franchisors may have a minimum net worth requirement.

Borrowers with good credit and collateral may be able to get a traditional loan from a bank or credit union. Most lenders are more likely to offer financing for a franchise business because they are associated with an established brand that has been proven in the marketplace. However, if you are interested in investing in a lesser-known brand such as an emerging franchise, or don’t have a stellar credit rating or collateral, a traditional lender may not be an option and you will need to look elsewhere for funding.

Personal Savings

When financing their new business venture, many franchisees will use personal savings like registered accounts such as Registered Retirement Savings Plans (RRSPs) and Tax Free Savings Accounts (TFSAs) to finance their new business. Some franchisees have used their homes as collateral to finance a franchise. But, the overall risk as well as tax implications often don’t make sense to finance a franchise in Canada in this manner.

Government Assistance Small Business Loans:

Small businesses (including franchises) looking to purchase or improve their assets for new or expanded operations could benefit from the Canada Small Business Financing Program (CSBFP).

This government-sponsored loan program offers up to $1,000,000 ($350,000 for equipment and leasehold improvements). The program only finances equipment, leaseholds and real estate and can’t be applied to marketing costs, royalties, and franchise fees.

A key benefit is that 85% of the loan is guaranteed to the lending Bank by the Federal government. This means less risk to you, the borrower.

Other benefits include:

Various Floating Rates, Fixed Rates and Blended Rate Principal Plus Interest and Principal including Interest repayment options available to the borrower.

Attractive loan repayment terms ranging from 7 years on equipment, 10 years on leasehold improvement, and up to 15 years on real property loans

Business Loan Insurance Plan is available (certain conditions may apply)

The lender (bank) doesn’t provide this free and will usually charge:

a loan document preparation fee of around $175

a $100 loan application fee

a one-time-only Federal Government registration fee (2% of the loan amount which may be included in the amount borrowed)

a 1.25% Administration Fee included as part of your interest rate (not much, but something you have to factor into your debt repayment calculations).

Thinking Outside the Box

When more conventional lending sources can’t produce enough cash to fund your franchise start-up costs, you may need to look beyond traditional methods. An investor such as a family member, friend, or business partner may be willing to offer you funding as well. However, allowing others to invest can come with some strings attached.

Investors may require the ability to make decisions about the business and most will expect a return on their investment, which will cut your profits at first. Still, it may be worthwhile to take on investors if it allows you to get the franchise up and running.

No matter what kind of financing you choose, it’s important to get all the facts in advance so that you’re not caught off guard when it comes time to repay loans or investors down the line.

A limited budget does not have to mean postponing or giving up your plans to buy a franchise. By finding the right financing options to meet your needs you can buy a franchise now and take charge of your future.